How to Improve Cash Flow: Top Strategies for Business Success

Learn effective ways to improve cash flow. Our expert tips on invoicing, expense control, and financing can boost your business’s financial health.

Tags

Feeling the cash flow squeeze? It's a pressure every business owner knows all too well, but the good news is, getting your finances back on track isn't some dark art. It really boils down to three things: getting paid faster, being smarter about your spending, and keeping a cash cushion for those inevitable surprises.

Nail these, and you're building a truly resilient business.

Building a Healthier Cash Flow for Your Business

It’s a classic trap: confusing profit with cash. You can have a record-breaking sales quarter on paper and still be scrambling to make payroll because your clients haven't paid yet. This is exactly why getting a handle on your cash flow—the actual money moving in and out of your bank account—is the single most important thing for your company's survival.

Think of it like this: profit is the endgame, but cash flow is the fuel that gets you there. Run out of fuel, and the entire journey grinds to a halt. Let's make sure your tank stays full.

Why Liquidity Is Your Greatest Asset

Right now, the smartest way to improve cash flow is to obsess over liquidity. Modern cash flow management is all about keeping enough cash on hand to weather any storm. This isn't just about surviving; it's about having the agility to pivot when the market throws you a curveball—whether it's a sudden sales dip or a supply chain disruption—without having to run for expensive emergency loans.

That cash buffer is what lets you confidently cover payroll and rent, no matter what. You can dig deeper into these cash management trends to see just how critical this has become for businesses everywhere.

"The key is to accept that even though things won’t be perfect, you can focus on doing your best to adapt to the fast-moving variables of... economics."

This really hits the nail on the head. You can't control everything, but you can build a financial foundation that's flexible enough to handle whatever comes your way.

Core Strategies for Financial Agility

Forget the high-level theory. We're going to break down the essential strategies into real, practical actions you can start using today.

- •Speed Up Your Receivables: We'll cover simple but powerful techniques to get your invoices paid faster, closing that painful gap between doing the work and having the cash in hand.

- •Master Your Expenses: This is about more than just cutting costs. It's about surgically removing waste and negotiating smarter deals with suppliers to keep more of your hard-earned money.

- •Forecast Like a Pro: Learn how to look ahead and predict your cash needs. When you can see shortfalls (and surpluses) coming, you can plan for them instead of reacting to them.

- •Put Technology to Work: We’ll show you how to use modern tools, like invoice automation from platforms like GetInvoice, to take the manual drudgery out of your finances and reduce costly human errors.

Before we dive into the details, let's look at a few quick wins you can implement right away.

Quick Wins to Improve Your Cash Flow

Sometimes you just need to see an immediate impact. The table below outlines some of the most effective strategies you can put into practice this week to give your cash flow a much-needed boost.

| Strategy | Primary Benefit | Implementation Effort |

|---|---|---|

| Switch to E-Invoicing | Get paid up to 3x faster | Low |

| Offer Early Payment Discounts | Encourages prompt payment from clients | Low |

| Review & Cut Non-Essential Costs | Immediately frees up cash | Medium |

| Negotiate Better Vendor Terms | Extends your payment cycles | Medium |

| Set Up a Business Line of Credit | Provides a ready cash buffer | Low |

These tactics are your first line of defense. They are relatively simple to execute but can have a surprisingly powerful and immediate effect on the cash available to your business. Now, let's explore each area in more depth.

Master Your Invoicing and Get Paid Faster

We’ve all been there. You have a profitable month on paper, but the bank account tells a different story. That gap between billing a client and actually getting paid can be a silent killer for cash flow, making it tough to cover payroll, rent, and other urgent expenses.

It's time to move beyond just sending invoices and start building a system that gets you paid on time, every time. The secret isn't complicated. It’s about making the payment process painless for your clients and airtight for you. When you’re clear, professional, and consistent, you’ll be amazed at how quickly payment behaviors can change for the better.

Ditch the Manual Work and Automate Your Invoicing

If you're still creating, sending, and chasing down invoices by hand, you're not just wasting time—you're leaving money on the table. Manual invoicing is a minefield of human error. A forgotten invoice here, a wrong due date there, and suddenly you’ve delayed a payment by weeks or even months.

This is where automation becomes your secret weapon.

Modern tools can completely overhaul your accounts receivable. Platforms like GetInvoice, for example, can plug into your existing systems and put the entire invoice lifecycle on autopilot, from creation to sending out polite payment reminders. By taking manual data entry out of the equation, you don't just get your time back; you guarantee that every invoice goes out correctly and on schedule.

Just look at the clarity an automated dashboard provides. You get a real-time, at-a-glance view of exactly where every invoice stands.

This kind of visibility means you can spot bottlenecks instantly and follow up on overdue payments without having to dig through a mountain of spreadsheets or sent emails. It's a proactive approach that’s essential for keeping your cash position healthy.

Simple, Actionable Tips for Faster Payments

Automating your system is the foundation. Now, let's layer on some smart, proven tactics to speed up your collections even more.

- •Offer Early Payment Discounts: A small carrot can work wonders. Offering a 1-2% discount for paying within 10 days gives clients a compelling financial reason to bump your invoice to the top of their pile.

- •Implement Fair Late Fees: Nobody likes them, but they work. Clearly state your late fee policy on every single invoice. Even if you never have to enforce it, its presence sets a professional boundary and discourages tardiness.

- •Make It Incredibly Easy to Pay: The fewer clicks, the better. Accept multiple payment methods, especially online options like credit cards and ACH bank transfers. The easier you make it for someone to give you money, the faster they will.

Key Takeaway: Convenience is king. One study found that businesses accepting online payments get paid much faster—in fact, 57% get paid the same day they send the bill. A smooth experience for your client puts cash directly into your account.

Thinking about payment friction is a great habit to build. It’s the same logic behind reducing cart abandonment in e-commerce—every barrier you remove brings you one step closer to getting paid.

Keeping Everything Organized and In Check

As your business scales, the sheer volume of invoices can quickly become chaotic. A messy system isn't just a headache; it's a direct threat to your financial health. Solid organization ensures that no payment ever slips through the cracks.

A reliable system helps you monitor due dates, keep up with partial payments, and maintain a clean audit trail for tax time. If you want to build a truly foolproof process, check out our deep-dive guide on how to keep track of invoices. Adopting this kind of systematic approach is how you turn invoicing from a reactive chore into a proactive strategy for boosting your cash flow.

Forecast Your Finances to Avoid Surprises

I've seen it happen more times than I can count: a business is profitable on paper but can't make payroll. It’s a terrifying and surprisingly common situation. Running a business without a cash flow forecast is like trying to drive across the country without a map or GPS. You might make some progress, but you're essentially flying blind.

The point of forecasting isn't to be a fortune teller. It's about shifting your mindset from reactive panic to proactive planning. A solid forecast gives you a heads-up on potential cash shortages (or even surpluses), giving you precious time to make smart moves instead of desperate ones.

Kicking Off Your First Forecast

Don't be intimidated; you don't need an advanced finance degree or fancy software to get started. At its heart, a cash flow forecast is just a projection of the money you expect to come in and go out over a set period. A 12-week forecast is a fantastic starting point.

To begin, you’ll need to pull together a few key pieces of data:

- •Your current cash balance: How much money is actually in your bank accounts today?

- •Projected cash inflows: List all the money you genuinely expect to receive. This includes invoices you’ve sent, recurring revenue, and realistic sales projections based on past performance.

- •Projected cash outflows: This is every single bill you anticipate paying. Think payroll, rent, supplier payments, software subscriptions, taxes—everything.

Once you have these numbers, pop them into a simple spreadsheet. List the weeks along the top row and your cash in/cash out categories down the side. This simple act alone will give you a level of clarity that is foundational to improving your cash flow.

For those just starting out, especially in industries like hospitality, a tool like a restaurant startup costs calculator can be invaluable for mapping out those initial expenses and preventing early surprises.

Play "What If?" to Build a Resilient Business

Your first forecast is your baseline—your most likely scenario. The real magic happens when you start exploring different possibilities. This is how you test your company's financial resilience and prepare for both the good and the bad.

Ask yourself some tough questions. What happens if your largest client pays 30 days late? What if your main delivery van breaks down? On the flip side, what if you land a huge project that requires you to hire two people right now?

A great forecast doesn't just show you one path; it illuminates several potential futures. By modeling these scenarios, you can create contingency plans, like securing a line of credit or building up a specific cash reserve, long before you actually need them.

This process transforms you from a scorekeeper just tracking money to a strategist actively managing it.

Using Your Forecast to Make Smarter Decisions

With a clearer picture of your future cash position, you can stop making decisions based on fear and start making them with confidence.

| If Your Forecast Shows... | You Can Confidently... |

|---|---|

| A cash surplus in 3 months | Plan a strategic investment, like a new marketing campaign or that equipment upgrade you've been wanting. |

| A potential cash crunch in 6 weeks | Proactively chase overdue invoices or negotiate better payment terms with a supplier before it's an emergency. |

| Consistent seasonal dips | Start building up cash reserves during your busy season to comfortably sail through the slower months. |

| Steady, predictable growth | Figure out the perfect time to bring on a new team member without putting a strain on your finances. |

This forward-looking view is what separates businesses that are constantly putting out fires from those that are thriving. You’ll start to see patterns you might have otherwise missed, allowing you to build a more stable, agile company that's ready for whatever comes next.

Smartly Manage Expenses and Vendor Relationships

Boosting cash flow isn’t just about getting paid faster; it’s also about being incredibly smart with the money going out. I've seen countless businesses unlock a surprising amount of cash just by getting strategic with their expenses and supplier relationships. It can be the difference that gives you the breathing room you need to really grow.

This isn't about being cheap—it’s about being intentional. A thoughtful approach ensures every dollar is an investment, not just another line item disappearing into operational overhead.

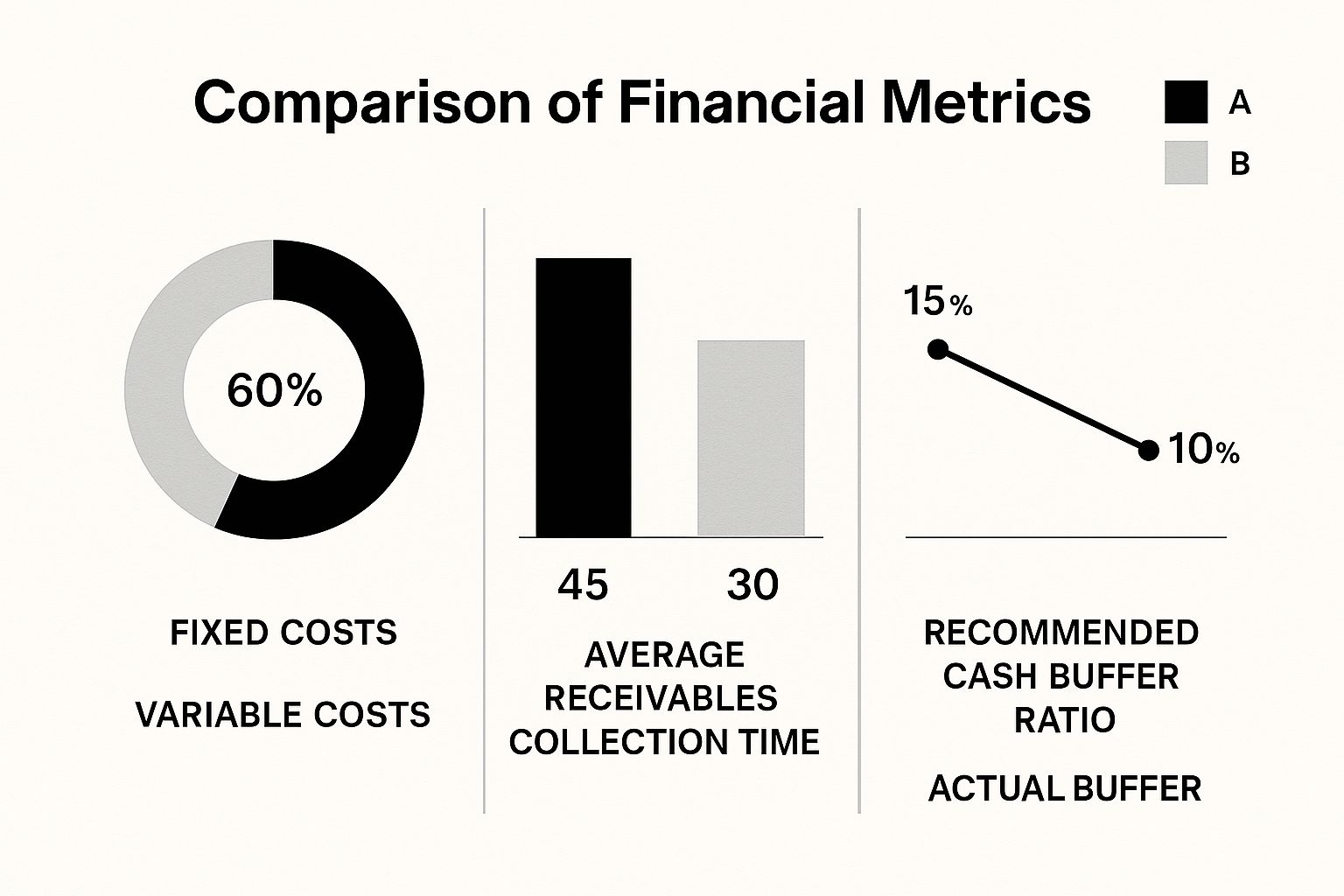

Look at this common scenario. It shows the all-too-familiar gap many businesses live with every day: the time it takes to collect your own invoices versus the time you have to pay your bills.

The image drives home a critical point. If your money is tied up in receivables for 45 days, but you have to pay your own bills in 30, you’re stuck in a permanent cash crunch. Let’s work on fixing that.

Conduct a Ruthless Expense Audit

First things first: you need to know exactly where your money is going. And I don’t mean a quick glance at your bank statement. It's time to pull up the last three months of expenses and get forensic. Scrutinize every single line item.

You’ll probably be surprised by what you find. I often see things like forgotten software subscriptions, overlapping services, or "miscellaneous" costs that have quietly ballooned over time.

Start by sorting your expenses into two piles:

- •Fixed Costs: These are your predictable, month-to-month expenses like rent, payroll, and essential software.

- •Variable Costs: These fluctuate with your business activity. Think marketing campaigns, raw materials, or freelance help.

Separating them like this instantly shows you what’s non-negotiable and where you have some wiggle room. More often than not, the biggest savings are hiding in your variable expenses.

Turn Vendor Negotiations into a Partnership

Your relationship with your suppliers shouldn't feel like a battle. When you start treating them like partners, you open the door to conversations that can radically improve cash flow. A primary goal here is to extend your payment terms, giving you more time to pay your bills without hurting your reputation.

Just think about the impact of shifting from NET 30 to NET 45 or even NET 60 terms. That single change can give you an extra 15-30 days to use your cash for payroll, inventory, or other critical needs.

Pro Tip: Don't just spring a request for better terms on a vendor. Frame it as a win-win. A loyal, long-term customer is an asset. You can point to your solid history of on-time payments as a reason they can trust you.

Here's a simple script I’ve seen work wonders. Feel free to adapt it:

"Hi [Supplier Name], we’ve really valued our partnership over the last [Number] years and appreciate your consistent service. As we work to align our payables with our own cash flow cycle, we’re looking to move our standard payment terms to NET 60. This would greatly help our financial planning and ensure we can continue to be a strong, reliable partner for you. Would you be open to discussing this?"

When you approach it this way, it’s not a demand; it’s a collaborative discussion.

Now, you have two core strategies for managing outflows: cutting costs and extending payment terms. Both are valid, but they serve different purposes. Let's break them down.

Expense Reduction vs Payment Term Negotiation

| Strategy | Pros | Cons | Best For... |

|---|---|---|---|

| Expense Reduction | - Immediately frees up cash. - Increases profit margins. - Fosters a leaner, more efficient operation. | - Can be time-consuming to audit. - May require sacrificing non-essential perks or services. - Could impact quality if cuts are too deep. | Businesses with high overhead, redundant subscriptions, or those looking for a quick, permanent boost to their bottom line. |

| Payment Term Negotiation | - Improves cash flow without cutting costs. - Strengthens vendor relationships when done collaboratively. - Provides predictable breathing room in your cash cycle. | - Success isn't guaranteed; depends on the vendor. - Doesn't reduce the total amount owed. - May require a strong payment history to be effective. | Stable businesses with solid vendor relationships looking to better align their payables with their receivables cycle. |

Ultimately, the best approach often involves a mix of both. A good expense audit cleans up the waste, while smarter payment terms give you the flexibility you need to operate smoothly.

Automate Your Payables for Total Control

While negotiating better terms is a game-changer, the way you manage the payment process itself is just as vital. A messy, manual accounts payable system is a recipe for missed early payment discounts or, even worse, late fees that eat away at your cash. This is where you can get a huge win from automation. If you want to dig deeper, see how you can automate accounts payable for better financial oversight.

Modern AP platforms give you a single dashboard to see all your bills, due dates, and discount opportunities. This visibility is power. It lets you strategically time your payments—paying early to snag a 2% discount when you have a cash surplus, or paying right on the due date to hold onto your cash longer when things are tight. That level of control is fundamental to intelligent cash management.

Use Smart Financing to Maintain Healthy Liquidity

Let's be real—even the most meticulously planned business can hit a cash crunch. It's not a sign you've failed; it's just the nature of the beast. Whether you're bridging a seasonal gap, seizing a sudden growth opportunity, or just trying to smooth out a lumpy payment cycle, smart financing is an incredible tool for improving cash flow.

The trick is to view financing as a strategic move, not a last-ditch cry for help. Thinking beyond a traditional bank loan is what separates a fragile business from a resilient one—one with the healthy liquidity needed to act fast and weather any storm.

This kind of preparedness is becoming more common. You can see a global trend of companies holding larger cash reserves, reflected in high money market fund balances. It’s a clear signal that businesses are prioritizing having liquid assets ready to deploy. For you, having access to the right kind of capital helps maintain that all-important buffer.

Beyond the Traditional Bank Loan

When most people hear "business financing," their mind immediately goes to a stuffy bank office and a classic term loan. But the financial toolkit available to small businesses today is so much bigger and more flexible. Exploring these alternatives can give you the wiggle room you need without saddling you with rigid, long-term debt.

To really improve business cash flow and keep your liquidity in a healthy spot, looking into various business loan options is a savvy move. The goal is always to find the perfect fit for your specific circumstances.

Here are a few of the most popular and effective tools I've seen businesses use to boost their liquidity:

- •Business Line of Credit: This is probably the most flexible option out there. Think of it as a super-powered credit card for your business, but with a much higher limit and usually a better interest rate. You can draw funds whenever you need them and only pay interest on what you actually use. It’s a perfect safety net for those "uh-oh" moments or unexpected opportunities.

- •Invoice Factoring: Are you constantly chasing down slow-paying clients? This can be a game-changer. Invoice factoring lets you sell your outstanding invoices to a factoring company at a small discount. You get a huge chunk of the invoice value right away, turning your accounts receivable into cash you can use now.

- •Merchant Cash Advance (MCA): If your business thrives on a high volume of credit and debit card sales (think retail or restaurants), an MCA might be a great fit. You get a lump sum of cash upfront in exchange for a percentage of your future card sales. Repayments are automatic and ebb and flow with your sales—a slow day means a smaller repayment.

Key Insight: Don't get fixated on finding the absolute lowest interest rate. Speed and flexibility are often far more valuable. A line of credit you can tap into instantly might be worth a whole lot more than a cumbersome loan that takes weeks to approve, even if the rate is a tad higher.

Choosing the Right Tool for the Job

Each of these financing options comes with its own set of trade-offs. The right choice depends entirely on why you need the cash and how your business actually runs. A mismatch here can easily create more problems than it solves.

For instance, a marketing agency that just finished a huge project and is waiting on a net-60 payment from a big client is a perfect candidate for invoice factoring. They have guaranteed money coming in, but they need cash today to make payroll. Factoring solves that immediate, short-term problem without creating long-term debt.

On the other hand, a retail shop gearing up for the holiday rush would get more mileage from a line of credit. They can use it to load up on inventory and then pay it down quickly as the holiday sales pour in.

You know what makes all of this easier? Having your financial house in order. Lenders love seeing clean, organized records. A clear invoicing process is a huge part of that. If your system is a bit chaotic, you might want to learn more about the benefits of invoice automation software and see how it can produce the kind of slick, professional records that give lenders confidence.

To make it even clearer, here’s a quick breakdown of where these options really shine.

| Financing Option | Best For... | Main Advantage | Key Consideration |

|---|---|---|---|

| Business Line of Credit | Ongoing, flexible access to cash for unexpected costs or opportunities. | You only pay interest on the amount you use. | Requires good credit and financial discipline to manage effectively. |

| Invoice Factoring | Businesses with reliable, but slow-paying, B2B clients. | Converts outstanding invoices into immediate cash. | You receive less than the full invoice amount; fees can be high. |

| Merchant Cash Advance | Businesses with high daily credit/debit card sales, like retail or restaurants. | Very fast funding; repayment is tied to your sales volume. | Can be expensive, with high effective interest rates (factor rates). |

Getting to know these distinctions is the first step. By matching the right tool to the right problem, you're not just borrowing money—you're building a financially agile company that can do more than just survive. You'll be ready to thrive.

Common Questions About Improving Cash Flow

Let's be honest, navigating business finances can feel like you're trying to solve a puzzle with a few pieces missing. As you work to get a better handle on your cash flow, it’s completely normal to have questions and wonder if you're making the right moves.

To help you out, I've pulled together some of the most common questions I hear from business owners about managing their money. Here are some straightforward answers to give you clarity and confidence.

What Is the Fastest Way to Improve Cash Flow?

Without a doubt, the quickest win is to speed up your accounts receivable. You've already earned the money; the goal now is simply to get it into your bank account as soon as humanly possible.

Start by sending out invoices the moment a job is done or a product ships. Don't wait for the end of the week or a set "billing day." That habit alone creates an unnecessary lag. Make sure your invoices are crystal clear, with the due date front and center, and offer a few simple ways to pay online.

One tactic that works like a charm is offering a small discount, like 2%, if they pay within 10 days. It gives clients a solid financial reason to put your invoice at the top of their pile. Finally, set up a friendly but firm automated follow-up sequence for overdue payments. These simple actions turn your completed work into cash much, much faster.

Can My Business Be Profitable but Have Poor Cash Flow?

Yes, absolutely. This is a classic—and frankly, dangerous—trap that many businesses fall into. It’s critical to understand that profit and cash flow are two very different things.

Profit is what's left on paper after you subtract your expenses from your revenue. It's an accounting measurement of your company's success over a period of time. Cash flow, on the other hand, is the real, tangible money moving in and out of your bank account.

Imagine you land a huge, highly profitable project. Fantastic! But what if the client has 90-day payment terms? Your accounting software shows a big profit, but your bank account is running on fumes. You still have to make payroll and pay rent. This is exactly why managing cash flow is vital for survival, while profit is the goal for long-term growth.

A business can be profitable and still go under because it runs out of cash. Think of profit as your destination and cash flow as the fuel in your tank. You can’t reach the destination if the tank runs dry.

How Often Should I Review My Cash Flow Statement?

The right answer depends on the rhythm of your business and its current financial state, but for most small businesses, a weekly review hits the sweet spot.

A weekly check-in gives you a real-time pulse on your finances. It helps you anticipate upcoming bills, see which clients have paid, and spot small issues before they snowball into major headaches. Making this a regular habit is one of the most powerful things you can do to proactively improve cash flow.

If your business is in a growth spurt or navigating a financially tight season, you might even need to check in daily. At the bare minimum, you must do a detailed monthly review. This lets you compare your actuals against your forecast and make smart, informed decisions for the month ahead.

Is Invoice Factoring a Good Idea for My Business?

Invoice factoring can be a lifesaver, but only in the right situation. It’s most effective when your main cash flow problem is consistently slow-paying B2B customers and you need cash right now for essential operations like making payroll or buying inventory.

The biggest plus is the speed and predictability it gives you. You can turn your outstanding invoices into cash in as little as 24 hours. The trade-off? That convenience comes at a cost. The factoring company will take a percentage of each invoice as their fee.

So, when does it make sense?

- •Good for: Businesses with long payment cycles, common in industries like manufacturing, wholesale, or professional services.

- •Not ideal for: Companies with razor-thin profit margins, where the factoring fees could wipe out your profit entirely.

It's a powerful tool, but think of it as a strategic fix for a specific problem, not a permanent part of your financial strategy. You have to weigh the cost of the fees against the immediate benefit of having cash in hand.

Ready to stop chasing payments and start automating your cash flow? GetInvoice connects directly to your inbox and client portals, using AI to extract invoice data automatically and sync it with your accounting software. Eliminate manual entry, get paid faster, and gain total visibility over your finances. Start your free trial of GetInvoice today!