Automate Bookkeeping And Reclaim Your Time

Ready to automate bookkeeping? Our guide shows you how to use the right tools to streamline finances, cut errors, and focus on growing your business.

Tags

Switching to automated bookkeeping is less about becoming a tech wizard and more about a simple mindset shift. You're not just doing the books anymore; you're supervising a smart system that does the heavy lifting for you. It’s about using modern tools to automatically grab, sort, and match up your financial data, giving you back hours of your day.

Your Starting Point for Automated Bookkeeping

Diving into automation can sound intimidating, but it’s really just an upgrade to your toolkit. Think of it as promoting yourself from data entry clerk to financial supervisor. Your expertise and judgment are still crucial—you’re just offloading the mind-numbing, repetitive tasks that drain your time and lead to mistakes.

The best way to start is by taking an honest look at your current process. Where are you losing the most time? Is it chasing down email attachments, manually keying in invoice details, or that dreaded month-end scramble to reconcile your bank statements? Finding these bottlenecks is your first real step.

Assess Your Current Bookkeeping Methods

Before you can build a better system, you need to understand what’s not working now. Pinpoint the tasks that are either the most time-consuming or the most likely to cause errors.

For most businesses, the pain points are pretty universal:

- •Manual Data Entry: This is the big one. Spending hours typing out details from PDFs or crumpled paper receipts is not only tedious but also a recipe for typos.

- •Document Collection: That constant hunt for invoices in your inbox, downloading statements from ten different portals, or trying to make sense of a shoebox full of receipts. It's a mess.

- •Reconciliation Gridlock: The end-of-the-month headache of matching every single bank transaction to an entry in your books. It can take hours, or even days.

Once you’ve identified your biggest time-sinks, you can set some real, tangible goals. For instance, you could aim to “eliminate 90% of manual invoice entry” or “reconcile bank transactions daily instead of just once a month.”

Here's a pro tip: The most successful automation projects don't try to boil the ocean. Focus on fixing your single biggest frustration first. Getting a quick, meaningful win builds momentum and makes the rest of the process feel much less daunting.

This focused approach is why the global financial automation market is booming, with a projected growth rate of over 14.2% a year through 2032. Businesses everywhere are realizing there’s a better way. You can explore more about these automation trends and their economic impact to see just how big this shift is.

Let's quickly compare the old way versus the new way.

Manual vs Automated Bookkeeping at a Glance

This table breaks down the fundamental differences between sticking with manual methods and embracing automation.

| Aspect | Manual Bookkeeping | Automated Bookkeeping |

|---|---|---|

| Time Spent | High (5-10+ hours/week) | Low (1-2 hours/week) |

| Cost | High hidden costs (time, errors, late fees) | Lower total cost (subscription + minimal time) |

| Accuracy | Prone to human error (typos, omissions) | High (data extracted directly, minimal errors) |

| Real-time Data | No, books are only current after month-end | Yes, financial data is updated daily |

| Scalability | Poor, more transactions mean more manual work | Excellent, system handles growth easily |

The contrast is pretty stark. Automation doesn't just save you time; it gives you a more accurate, up-to-date picture of your business's financial health, which is invaluable for making smart decisions.

Is Your Business Ready for Automation?

Honestly, most businesses are ready, even if they don't feel like it. The tools needed for a great automated system are more user-friendly and affordable than ever. Modern cloud accounting platforms like Xero are designed to give you a clear, simple overview of your finances.

Take a look at a typical Xero dashboard.

Right away, you can see your bank balances, who owes you money, and your overall cash flow. It transforms confusing data into simple, actionable insights. This kind of clarity is one of the biggest perks of an automated system.

Still not sure? Run through this quick checklist:

- •Do you handle more than 20-30 invoices or receipts each month?

- •Do you use online banking for your business?

- •Are you still relying on spreadsheets or old desktop software?

- •Do you wish you had a real-time snapshot of your finances?

If you answered "yes" to even two of those questions, you're a perfect candidate for automation. The tools available today are built for exactly these situations, ready to turn your manual chaos into a smooth, reliable workflow right from the start.

Finding the Right Automation Tools for Your Business

Let’s be honest, picking the right software to automate your bookkeeping isn’t about chasing the biggest name brand. It's about finding the tool that actually fits how you do business. The market is packed with options, but the best choice is always the one that molds to your daily operations, not the other way around.

Before you get pulled into a vortex of feature lists and confusing pricing tiers, let's zero in on what truly matters. You're not just buying software; you're investing in a solution that will solve your specific headaches and grow alongside you. This isn't just a small trend, either. The automated bookkeeping market is exploding—it was valued at around $15 billion in 2025 and is expected to grow by 15% every year, potentially hitting $50 billion by 2033. It’s clear that businesses are fundamentally changing how they manage their money. You can discover more about this growth and its key drivers.

Evaluate Core Integration Capabilities

Here’s the most important thing to look for: how well does the tool play with the other software you already use every day? If a bookkeeping platform can't connect to your bank, payment processor, or sales channels, it’s just creating more manual work. That completely defeats the purpose of automating in the first place.

Take a moment to map out your workflow. If you're a freelance designer, you absolutely need something that syncs perfectly with Stripe or PayPal. Run a local café? Your tool must connect to your point-of-sale system, like Square or Toast, to pull in daily sales data without you lifting a finger.

Look for these non-negotiable integrations:

- •Bank Feeds: Real-time, direct connections to your business bank accounts and credit cards are a must-have.

- •Payment Gateways: Make sure it works with platforms like Stripe, PayPal, or Square so revenue is recorded automatically.

- •Sales Platforms: If you’re in e-commerce, it’s critical that it integrates with Shopify, WooCommerce, or Amazon to track sales and fees accurately.

Scalability and User-Friendliness

The business you run today isn't the one you'll be running in a year. The right tool needs to keep up. A freelancer might only have 30 transactions a month right now, but a growing online store could easily be juggling 3,000. You have to ask: can this software handle that kind of jump in volume without lagging or jacking up the price?

Just as important is how easy it is to actually use. A clunky, complicated system with a steep learning curve will only lead to frustration and pushback from your team. You want a platform with an intuitive dashboard and clear navigation, something like the interface offered by QuickBooks.

This screenshot is a great example of how modern tools can make complex financial data feel simple and visual. You should be able to understand the health of your business at a glance. The right tool feels empowering, not intimidating. To get a feel for what’s possible, it’s worth looking at how other business areas are being transformed. For instance, there are plenty of proven strategies and AI tools for automation in sales that show the power of this approach.

All-in-One Platforms vs. Specialized Apps

When it comes down to it, you have two main paths you can take: an all-in-one platform or a curated mix of specialized apps.

An all-in-one platform like QuickBooks or Xero tries to do it all—invoicing, expense tracking, payroll, and reporting. For most businesses that want a single source of truth for their finances, this is often the smartest choice.

On the flip side, a specialized app is designed to excel at one specific job, like capturing receipts or managing expenses. You might pair one of these with a simpler accounting tool if you have a very particular, high-volume need. The key is making sure it integrates seamlessly with your main accounting system. We take a closer look at how these systems can work together in our guide on accounting process automation.

Ultimately, the right choice really hinges on your business's complexity and whether you prefer having everything under one roof or building your own custom-fit tech stack.

Alright, let's ditch the shoeboxes full of faded receipts and stop the endless scrolling through your inbox for that one missing invoice. We're going to build a smart system to catch every single financial document automatically. This is the foundation of automated bookkeeping, and it's where you start getting your time back.

The whole point is to create a funnel that sends every supplier invoice, coffee shop receipt, and software subscription payment straight into your bookkeeping software. No more manual data entry. You're shifting from a chaotic, reactive paper chase to a smooth, proactive digital workflow.

We'll tackle this with two simple but powerful tools: a dedicated email address for all things financial and a slick mobile app for on-the-go scanning.

Set Up a Dedicated Receipts Email

Think about your main inbox right now. It's probably a mix of client emails, marketing newsletters, and a few dozen other things. Important invoices can get buried in minutes.

The easiest fix is to create a separate email address just for financial documents. Something like receipts@yourbusiness.com or invoices@yourbusiness.com is perfect. This carves out a clean, quiet space for your financial paper trail, completely isolated from the daily noise.

Once you have that email, the next move is to hook it up to your accounting software. Most modern platforms, including our own at GetInvoice, can connect to an inbox or give you a unique email address to forward things to. All you have to do is set up an automatic forwarding rule, and every email that hits your "receipts" account will zap right into your books.

Here's how to make it work in the real world:

- •Update Your Supplier Profiles: Jump into your accounts for web hosting, software subscriptions, or utilities and switch the billing email to your new one.

- •Get Your Team On Board: If you have employees making purchases, tell them this is the new go-to email for any sign-ups or receipts they need to submit.

- •Nudge Your Vendors: The next time a freelancer or small vendor sends you an invoice, just reply and ask them to use the new address going forward. It's a small request, and most people are happy to help.

This one change makes a huge difference. Documents start flowing to you, right where you need them, instead of you having to hunt them down.

Master the Mobile App Scanner

What about all the paper stuff? The client lunches, the emergency office supply runs, the gas receipts—these are the ones that always seem to vanish. This is where a good mobile scanner app becomes your secret weapon.

Most top-tier accounting software includes a mobile app with a receipt scanning feature. It's as simple as it sounds: you open the app, snap a quick photo of the receipt, and boom—it's uploaded. The app's built-in Optical Character Recognition (OCR) technology then reads all the key details for you.

I see this all the time: people let physical receipts pile up in their wallet or on their desk to scan "later." That completely defeats the purpose. The trick is to build the habit of scanning the receipt the moment you get it. Do it before you even walk out of the store. It takes 10 seconds and guarantees you'll never lose another one.

By the time you get back to your office, the expense is already logged and waiting. No more sorting through a pocketful of crumpled paper at the end of the month. You'll have a perfect digital copy of every single transaction.

When you combine these two methods—the dedicated email for digital stuff and the mobile app for physical receipts—you create a capture system that's pretty much foolproof. No matter how a financial document comes at you, you've got a simple, automated path to get it right into your books. This is the first, most critical step to taking back your time.

Using AI to Intelligently Extract and Categorize Your Financial Data

Alright, you’ve got a steady stream of invoices and receipts flowing into your system. Now for the magic. This is where we stop just collecting documents and start making them work for us, all thanks to some clever AI that acts like a junior bookkeeper who never sleeps.

At its core, this whole process relies on Optical Character Recognition, or OCR. It’s the technology that lets your software read the text on your documents—even if it’s a blurry photo of a receipt from your phone. But modern tools like GetInvoice take it a step further. They don't just read the text; an AI layer on top actually understands it. We get into the nitty-gritty of the tech in our guide to invoice OCR software.

This combo of OCR and AI is what enables the system to intelligently pull out the key details, like:

- •The vendor’s name (think "Staples" or "Amazon Web Services")

- •The total amount and transaction date

- •The invoice number for easy tracking

- •Individual line items that tell you exactly what was bought

Getting started is less about complex technical setup and more about providing a little guidance. Just think of it like training a new assistant. The software will take its best shot at the first few documents, and you just need to check its work.

Fine-Tuning the AI for Pinpoint Accuracy

When you first begin, the AI might pull the vendor and total from a new invoice perfectly but leave the expense category blank. No problem. You simply point it to the right place in your chart of accounts—for instance, telling it that a payment to Google should be categorized as "Advertising."

The AI is designed to learn from you. The very next time a Google invoice pops up, it will remember your last move and suggest "Advertising" for you. Once you’ve confirmed this a couple of times, it becomes confident enough to categorize these transactions all on its own, no review needed. This simple feedback loop is all it takes to "train" the system, and it gets incredibly accurate, fast.

This learning ability is a huge reason why automation is taking over. The data speaks for itself: the percentage of invoices entered into accounting systems by hand dropped from 85% in 2023 to just 60% in 2024. And it's not slowing down. It’s projected that 80% of firms will be using in-house AI for financial decisions by 2026. If you're interested, you can explore more key automation statistics to see just how fast things are moving.

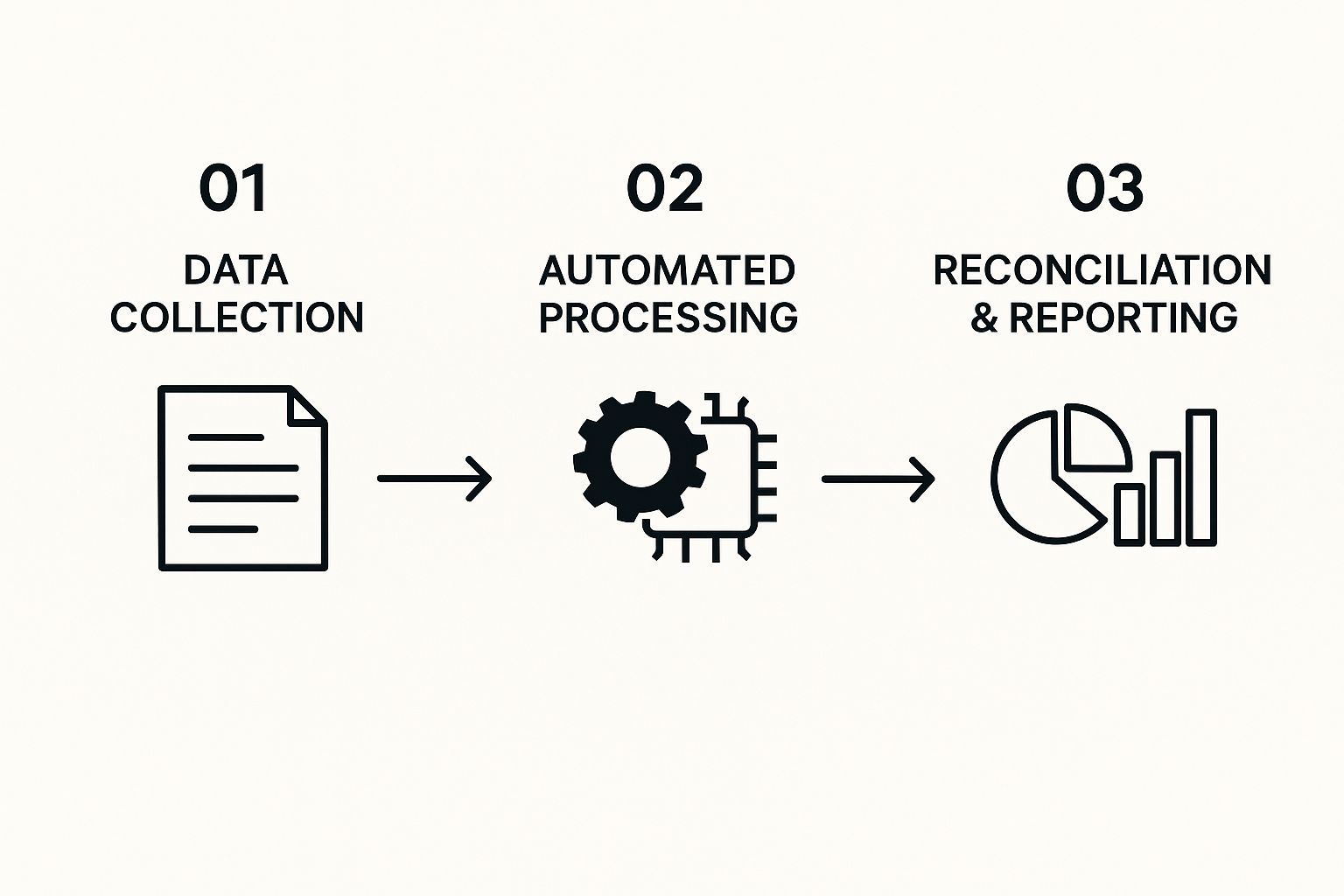

This infographic gives a great visual of how a document travels from being a piece of paper to a fully reconciled entry in your books.

As you can see, each step builds on the last, turning a pile of raw data into polished financial reports with surprisingly little effort on your part.

Creating Rules to Handle Your Recurring Expenses

Beyond letting the AI learn on its own, you can also be proactive by setting up your own rules. This is where you get to tell the system exactly how to handle certain transactions every single time, giving you perfect consistency and keeping your books spotless.

Key Insight: Taking a few minutes to create specific automation rules is one of the highest-impact things you can do. It transforms a smart tool into a fully reliable engine for your financial operations, saving you countless hours of manual work down the road.

These rules aren’t just about basic categorization; they give you precise control over your financial data. Honestly, they’re the backbone of any truly automated bookkeeping setup.

High-Impact Automation Rules to Set Up First

To get the biggest bang for your buck right away, I always recommend starting with rules for your most common and predictable transactions. Here are a few examples that will make an immediate difference.

| Transaction Type | Suggested Rule | Benefit |

|---|---|---|

| Software Subscriptions | If vendor is "Microsoft" or "Adobe," categorize as "Software & Subscriptions." | Ensures all your recurring SaaS costs are grouped correctly without you having to touch them each month. |

| E-commerce Payouts | If description contains "Shopify Payout," categorize as "Sales" and split out fees. | Automatically separates your gross sales from transaction fees, giving you an accurate picture of your true revenue. |

| Freelancer Payments | If vendor is "Upwork" or a specific contractor's name, categorize as "Contractor Expenses." | Keeps your freelancer and outsourced labor costs consistently tracked, which is a lifesaver for budgeting and taxes. |

| Utility Bills | If vendor is "City Water" or "National Grid," categorize as "Utilities." | Prevents utility payments from being miscategorized and makes it incredibly easy to track your core operational costs. |

By setting up these rules, you're essentially building a system that doesn't just guess—it knows. Before long, you'll find that almost all of your routine transactions are handled automatically, leaving you with only the occasional oddball item to review. This is how you change bookkeeping from a daily chore into a quick, supervisory task.

Tying It All Together: Automated Bank Reconciliation

This is the final, most satisfying piece of the puzzle. When you connect your bookkeeping software directly to your bank, you officially graduate from chasing down paperwork to simply supervising a smooth, consistent flow of financial data. The dreaded month-end crunch? It's about to become a distant memory. The magic starts by setting up a live bank feed.

Think of this connection as a secure pipeline. It pulls your bank and credit card transactions straight into your accounting software, usually every single day. The setup is typically a quick, one-time thing you do right inside your software. Once that link is live, you'll see every debit and credit pop up automatically, just waiting to be matched.

Let the Software Do the Heavy Lifting with Smart Matching

Here's where the system's intelligence really flexes its muscles. Your software now has two sets of information to work with: the receipts and invoices you've been sending in, and the transaction data streaming from your bank. Its primary job is to play matchmaker.

Let's walk through a real-world example. Say you get your monthly $25 invoice from a tool like Asana or Trello. You forward it to your dedicated bookkeeping email, and it lands in the system. A few days later, the $25 charge hits your bank feed. The AI notices the identical amounts and vendor names, then suggests a match. All you have to do is click "OK."

The system gets smarter over time, too. After you confirm a few transactions from the same vendor, it learns your habits. Soon, it will start matching them for you automatically, no approval needed. This daily, automated process gives you a constantly updated and remarkably accurate picture of your business's financial health.

Just look at how clean and simple this can be in a tool like FreshBooks.

An interface like this transforms what used to be hours of tedious data entry into a quick, visual check-in. It clearly shows what needs your attention and what's already been taken care of.

Handling the Oddballs: Where a Human Touch Still Wins

Let's be realistic—no system is 100% perfect, and that's okay. You'll always have a few transactions that need a bit of manual intervention. These are the exceptions that prove how well the rule works for everything else.

You might run into scenarios like:

- •Bank Fees: That small monthly service charge from your bank that doesn't come with an invoice.

- •Partial Payments: When a client pays a portion of an invoice, meaning you have to split the payment application.

- •Bundled Deposits: A single deposit from a payment processor that covers payments from several different customers.

These are surprisingly easy to handle. For a bank fee, you can just create a new expense for it on the fly. For those partial or bundled payments, most modern software lets you easily match a single transaction to multiple invoices. The key takeaway is that you're only actively managing these few outliers, not every single transaction that comes through. We dig into managing these tricky situations in more detail in our guide to invoice processing automation.

My Pro Tip: I always tell my clients to set aside just 10-15 minutes every couple of days to review their bank feed. This "little and often" approach keeps your books pristine and prevents a backlog from ever forming. You’ll spot any issues right away and roll into month-end with your books already 99% done.

This constant, real-time sync is the ultimate goal of automated bookkeeping. It builds incredible confidence in your numbers without the soul-crushing grind. And if you want to make your data even cleaner, you can explore various strategies for automated payment processing to simplify how money flows into your business. When you embrace these systems, your financial reports stop being a historical artifact and become a living, breathing tool you can trust to make smart decisions.

Turning Automated Data into Powerful Business Insights

Alright, you've done the hard work of setting up your automated bookkeeping. Now comes the fun part—the real payoff. You can finally stop drowning in data entry and start paying attention to what the numbers are actually telling you. This is where you go from just collecting data to using it to make genuinely smarter decisions.

Forget about those painful hours spent exporting files and wrestling with spreadsheets. With everything configured, pulling up-to-the-minute reports like a Profit & Loss or a Cash Flow statement is as easy as clicking a button. These aren't just month-end chores anymore; they're on-demand tools that give you a real-time pulse on your business.

Customizing Reports to Track What Matters

Standard reports are a solid starting point, but the real magic happens when you tailor them to your specific business. Every business has its own unique vital signs, the metrics that scream success or signal trouble ahead. Your new system lets you zero in on these Key Performance Indicators (KPIs) with custom reports.

For instance, if you run an e-commerce store, you’ll probably want to keep a close eye on your Cost of Goods Sold (COGS) as a percentage of revenue each week. For a marketing agency, a better report might compare monthly recurring revenue directly against client acquisition costs. It's all about focusing on what drives your business.

You can typically build these reports by:

- •Filtering by Category: Isolate your "Marketing" or "Operations" expenses to see exactly where the money is flowing.

- •Comparing Time Periods: Instantly see how this month stacks up against last month or the same time last year to spot trends early.

- •Tracking Specific Items: Drill down into a single revenue stream or expense to understand its true impact on your bottom line.

This kind of flexibility turns your financial data from a static, historical record into a living, breathing tool for strategic planning.

Scheduling Reports for Proactive Oversight

One of the most valuable habits you can build is setting up automated report delivery. Instead of needing to remember to check in, you can have the most important information come directly to you.

Most modern accounting platforms let you schedule key reports to be automatically emailed to you or your team. Imagine getting a snapshot of your cash flow in your inbox every Monday morning. Or a detailed P&L statement landing on your desk on the first of every month, without you lifting a finger.

A Personal Tip: I always have my clients schedule two core reports. First, a weekly Cash Flow summary. This keeps your day-to-day liquidity front and center. Second, a monthly "Budget vs. Actual" report. This is your reality check—it shows exactly where you’re over or under budget, letting you make adjustments quickly before small issues become big problems.

This proactive approach is what really separates automated bookkeeping from the old manual slog. You stop reacting to what happened last month and start staying constantly informed, giving you the confidence to guide your business forward.

From Data Points to Strategic Decisions

Ultimately, this is all about using insights to take meaningful action. When you automate bookkeeping, you create a powerful feedback loop that connects your day-to-day operations with your high-level strategy.

Here’s how this plays out in the real world:

- •Spot a Trend: Your automated P&L report shows that your "Software Subscriptions" category has crept up by 15% month-over-month.

- •Dig Deeper: You run a quick, detailed expense report for just that category and discover you’re paying for two redundant project management tools.

- •Take Action: You cancel the unnecessary service, instantly trimming overhead and boosting your net profit.

This whole cycle—from spotting an issue to fixing it—can happen in minutes instead of weeks. That’s the real advantage of having clean, accessible, and up-to-date financial data at your fingertips. You stop guessing and start knowing, turning your financial system into one of your most valuable strategic assets.

Answering Your Top Questions About Automated Bookkeeping

Switching to automated bookkeeping can feel like a big leap, so it's completely normal to have a few questions swirling around. Let's walk through some of the most common concerns I hear from business owners. My goal is to give you the clear, straightforward answers you need to feel confident about making the move.

"Is My Financial Data Really Secure?"

This is always the first question, and honestly, it should be. You're right to be cautious with your financial information.

The good news is that established automation platforms are built with security at their core—often far more robust than a spreadsheet saved on a laptop. They use enterprise-level protections to keep your data locked down.

When you're evaluating a tool, make sure it has:

- •Solid Data Encryption: Your information should be encrypted both in transit (as it moves) and at rest (when it's stored on their servers).

- •Compliance with Privacy Standards: Look for mentions of GDPR or similar regulations. This shows they take data privacy seriously.

- •Secure, Read-Only Connections: The best tools use direct bank feeds and API integrations that only have "read" access. This means the software can see your transactions to categorize them, but it has absolutely no ability to touch or move your money.

It’s a lot like your online banking portal—built from the ground up with security as the top priority.

"What's the Actual Cost?"

It’s easy to get caught up comparing a monthly software fee to the "free" way you're doing things now. But that's not the full picture. The hidden costs of manual bookkeeping—your time spent on tedious data entry, the stress of tax season, or the price of fixing one small but costly mistake—add up fast.

The real return on your investment isn't just about saving money on the software itself. Think about it this way: if you save 10 hours a month and you value your time at $50/hour, that’s $500 in reclaimed value. Subtract a $50 monthly software fee, and you're still $450 ahead. That's time you can pour back into growing your business.

"How Long Will It Take Me to Learn This?"

I get it, nobody wants to spend weeks learning a complicated new piece of software. Thankfully, the learning curve for modern bookkeeping tools is surprisingly gentle. They're designed for entrepreneurs and business owners, not just accountants.

There's a little bit of setup at the beginning, of course—you'll need to connect your bank accounts and maybe set a few initial rules. But most people I've seen adopt these tools feel like they've got the hang of it within the first week.

Just plan for a brief adjustment period. You’ll spend a little extra time double-checking what the AI suggests. This initial effort is what teaches the system your business's specific patterns, and it pays off incredibly quickly as it becomes more accurate and needs less of your attention.

Stop chasing invoices and start making smarter decisions. GetInvoice plugs directly into your workflow, using AI to capture and categorize every financial document automatically. Find out how much time you can save.